Subsidized vs Unsubsidized

Subsidized loans government pays the interest. When the person is in school or the economic hardship deferments. Unsubsidized is the responsibility of the borrower. Subsidized is the least expensive option. During subsidized responsibility to repay back the government is suspended as long as you're in school half time. Payments are delayed until the end of grace period after graduation. Subsidized loans the government pays the interest as it accrues. And Unsubsidized loans increase if the interest is not paid.

Gov vs Bank

Federal loans funded by government, private loans are from the bank. Federal loans include many benefits such as fixed interest rates and income based repayment plans. Bank loans are usually more expensive. Federal loans pay when graduate and/or change your enrollment status to less than half time. Bank loans you pay while still in college. Dont need a credit check for most federal loans. Interest rate is fixed and lower than private loans. You might need a cosigner for bank loans. Bank loans are not subsidized. Federal loans you maybe able to postpone or lower your payments. There is no prepayment penalty fee for federal loans

Interest Rates

Subsidized- 4.66%

Unsubsidized- 4.66%

Bank loans- 5.99%-11.24%

Subsidized loans government pays the interest. When the person is in school or the economic hardship deferments. Unsubsidized is the responsibility of the borrower. Subsidized is the least expensive option. During subsidized responsibility to repay back the government is suspended as long as you're in school half time. Payments are delayed until the end of grace period after graduation. Subsidized loans the government pays the interest as it accrues. And Unsubsidized loans increase if the interest is not paid.

Gov vs Bank

Federal loans funded by government, private loans are from the bank. Federal loans include many benefits such as fixed interest rates and income based repayment plans. Bank loans are usually more expensive. Federal loans pay when graduate and/or change your enrollment status to less than half time. Bank loans you pay while still in college. Dont need a credit check for most federal loans. Interest rate is fixed and lower than private loans. You might need a cosigner for bank loans. Bank loans are not subsidized. Federal loans you maybe able to postpone or lower your payments. There is no prepayment penalty fee for federal loans

Interest Rates

Subsidized- 4.66%

Unsubsidized- 4.66%

Bank loans- 5.99%-11.24%

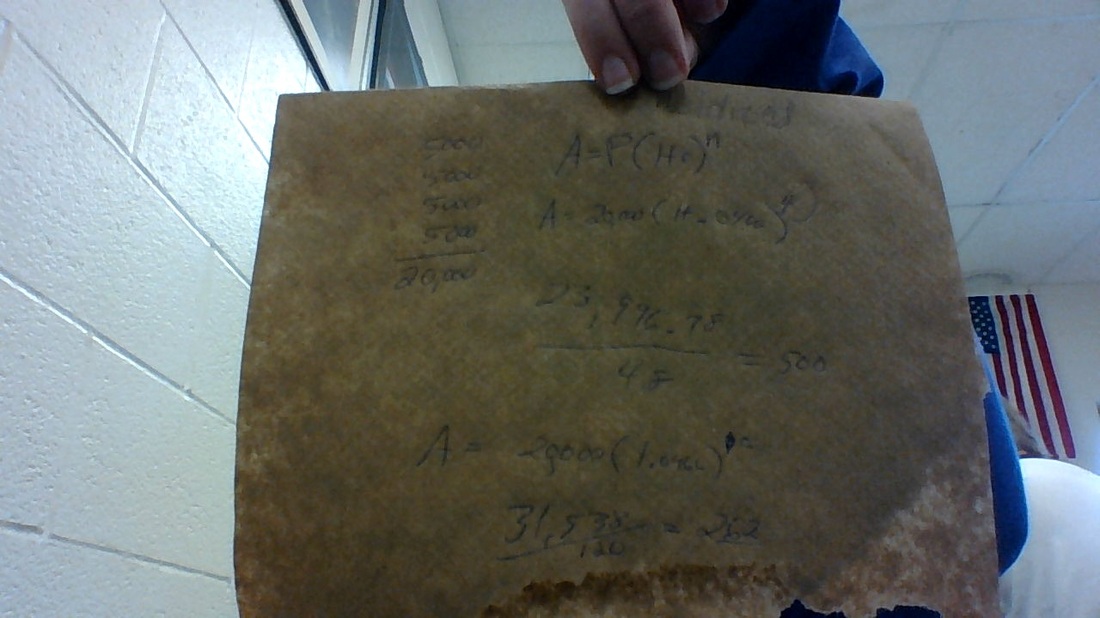

In the picture above it shows how much I would have to pay back in students for 4 years and 10 years. It is kind of hard to see but for 4 years I would have to pay back $500 a month. Then for 10 years I would have to pay back $262 a month. So clearly paying back more money is cheaper in a sense.

RSS Feed

RSS Feed